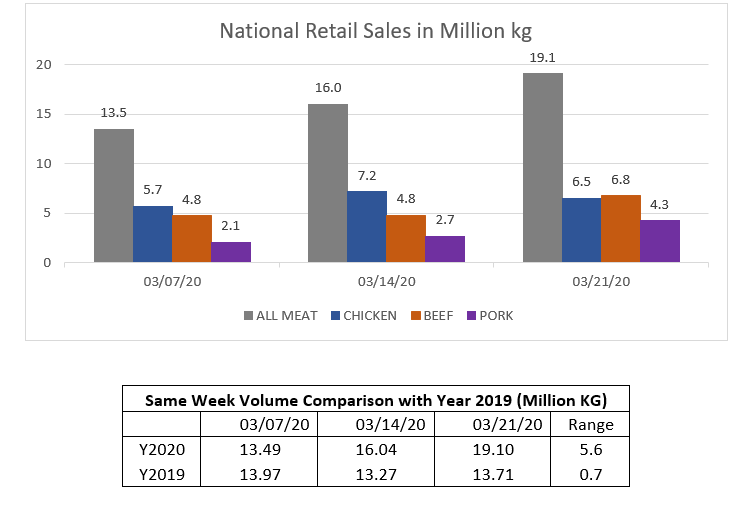

Stage 1 – First Three Weeks in March 2020: Sharp Increase in Volumes

Canada started to implement social distancing at the national level from mid-March 2020. In the first week’s lockdown from March 15th, 2020 to March 21st, 2020, the total meat sales were 19.1 million kilograms (Mkg), a 20 percent increase compared to the week before (16 Mkg). This increase was mainly due to the consumption in beef (2.0 Mkg↑) and pork (1.6 Mkg↑), while chicken’s volume decreased by 0.7 Mkg. In the week before the lockdown, which ended on March 14th, 2020, the total meat consumption was also increased by 2.5 Mkg compared to week ending on March 7th, 2020. In this week, both chicken and pork were the main drivers.

In 2019, the same three weeks’ total meat consumptions varied within a small range. The difference between the maximum and minimum consumptions during the three weeks was 0.7 Mkg. However, in 2020, this number was 5.6 Mkg. The three weeks’ unusual changes in meat consumption suggested that when the pandemic started to become severe in Canada, consumers tended to stockpile more meat.

This phenomenon can be explained by two reasons: first, meat is the food that can be easily preserved. Stockpiling enough meat at home can minimize the time for doing groceries and being exposed in public area, therefore minimize the risk of being infected. Second, consumers’ behavior was also influenced by panic, which pushed them to buy as much food as possible in order to counter the effect of a potential food shortage.

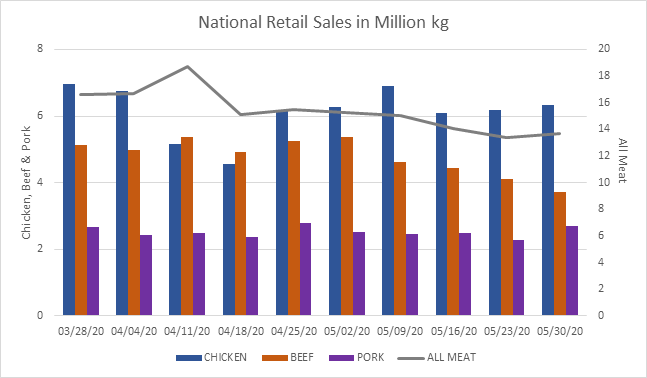

Stage 2 – Late March to Late May: Sales Decrease in Fluctuation

Since the beginning of the pandemic, employees in nine meat processing plants in Canada tested positive. From March 29th to April 24th, six plants closed temporarily for either two weeks, or without a reopening date. Even after the reopening, plants decided to reduce the number of workers per shift to practice social distancing. Beef was impacted most during this time. Four beef plants in Alberta and Quebec were affected by Covid-19, among them two plants were shut down temporarily on Apr 20th and May 13th, and another reduced the shift to one person per day in early May.

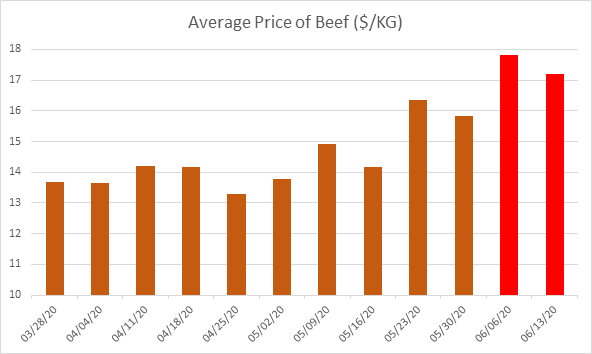

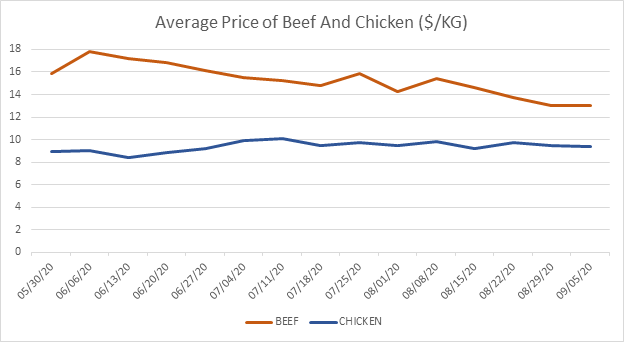

The influence of the supply chain’s disruption on beef was not too obvious until May 2nd. From late March to early May, consumers’ beef stockpile was not as crazy as when the pandemic started. Retails also had some plans to deal with the first week’s plants’ shutdown. However, after May 2nd, the beef supply chain’s disruption could be easily observed from the decreasing sales and increasing average price. In the next 6 weeks, beef’s retail volumes decreased by 40 percent. The average price increased from $13.8/kg to 17.2/kg, with the highest average price increased to $17.8/kg in the week ending on June 6th.

Beef’s consumption variation from late March to late May also caused the sales’ decrease in total meat during this period. Pork’s sales were more stable, although one pork plant in Ontario closed for two weeks in late April.

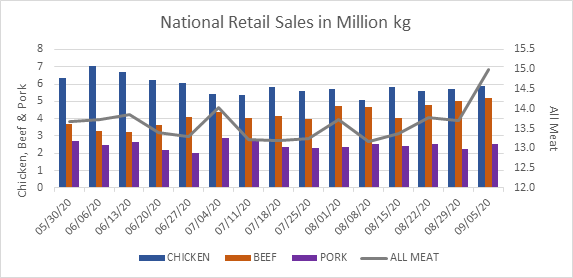

Stage 3 – Late May to Present: Consumption Level Comes Back to Normal Gradually

Total meat consumption started to come back to normal and has been stable since late May with consumers mostly choosing between chicken and beef. From late May to mid-June, the shutdown of beef plants triggered the increase of beef’s average price and dragged down beef’s volume. At the same time, chicken’s price decreased from $9.05/kg to $8.44/kg, therefore, bringing up chicken’s volume. After mid-June, when the influence of beef plants’ closure had been contained, beef’s price started to fall. However, during this time, chicken’s price rose. The impact is that chicken and beef consumptions varied in the opposite direction, but their compound effect makes the total meat consumption stabilize.

{kind=link}