In a recent data snapshot analysis, Valoral Advisors’ Roberto Viton reveals that venture capital dedicated to the agrifood sector represents only 2% of the global investment pool. Despite the growth of agrifood-focused VC funds from 42 in 2013 to over 280 by the third quarter of 2023, this expansion has slowed in recent years.

Viton anticipates 2024 to be a challenging year for the agrifood industry, foreseeing increased struggles for companies and potential closures. He notes a trend of startup founders engaging in discussions about mergers and consolidations to navigate the tough times ahead.

Efforts towards more efficient food production necessitate substantial capital, and Viton identifies four factors driving the growth of agrifood-focused VC funds: limited planetary resources and climate change impacts, population growth and evolving diets, geopolitical and economic factors like war and inflation, and technological breakthroughs across various industries.

Despite the positive trajectory, Viton emphasizes that the growth in agrifood investments was feasible due to starting from low levels, and the sector is still in its early stages. The infusion of capital is driven by the potential for attractive returns, with larger asset managers, specialized managers, and banks developing new strategies in the agrifood space.

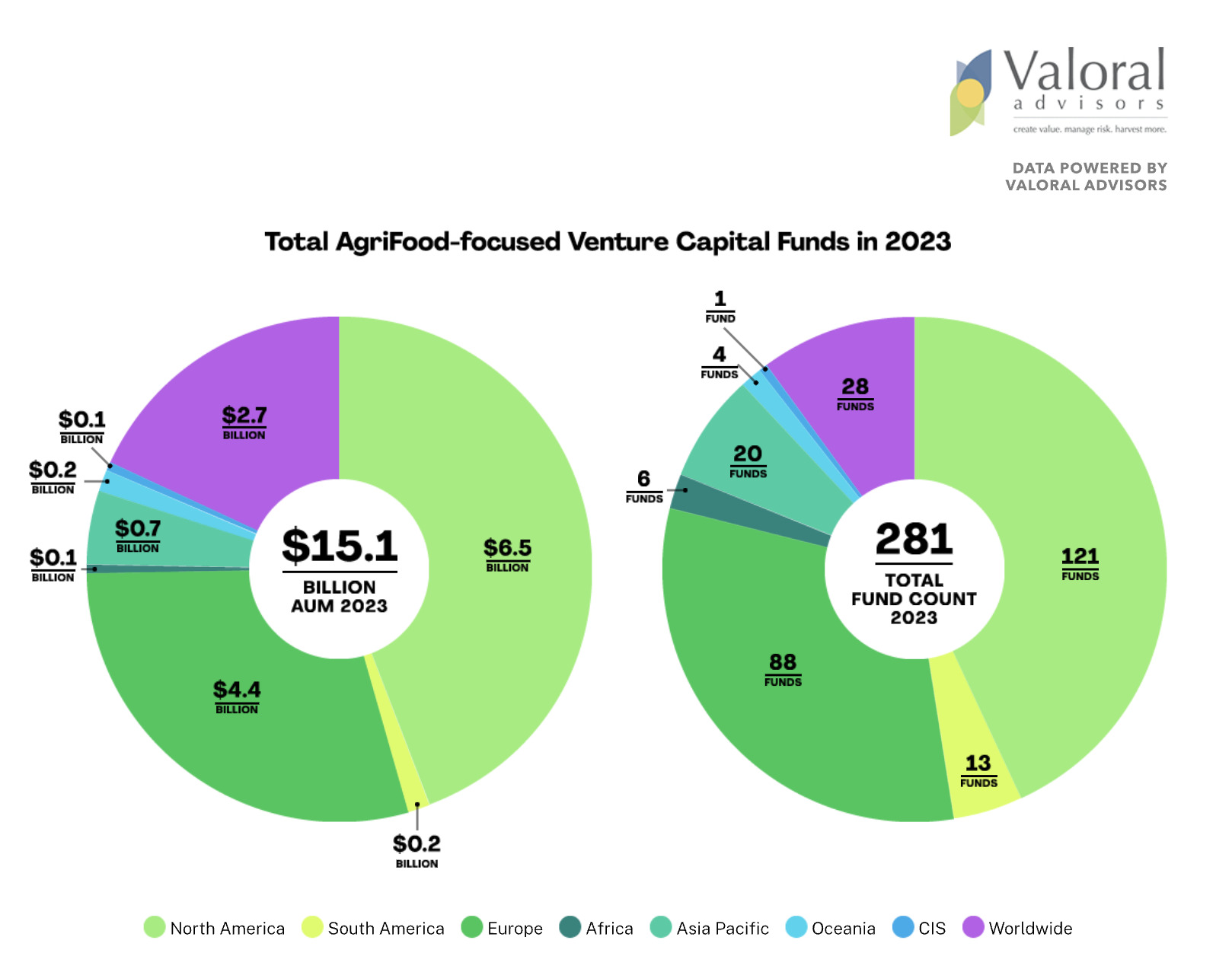

In 2023, agrifood-focused venture capital funds managed assets totaling $15.1 billion. Although the number of agrifoodtech VC funds increased, the growth rate was a modest 2.5%, contrasting sharply with the 32% increase observed from 2018 to 2019. Viton attributes the challenges faced by new fund managers in recent years to the slower pace of fund growth.

North America and Europe dominate agrifood’s assets under management, with $6.5 billion and $4.4 billion, respectively. Viton highlights that most investors and capital are concentrated in these regions, given their advanced innovation and talent. He anticipates a gradual shift towards increased activity in Latin America, Africa, and the Asia-Pacific regions over time, acknowledging that this evolution will take time.

{kind=link}